This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Home forfeiture actions, including completed foreclosure sales, shortsales, and deed in-lieu-of- foreclosure actions also grew by 26.8% were “combination modifications,” where interest rate reductions and term extensions are applied to a loan to help bring down a borrowers mortgage payment.

” Forbearance allows homeowners to defer mortgage loan monthly payments due to financial hardships, remaining in their homes. Critically, during the pandemic, a share of borrowers in forbearance kept paying their mortgage loans monthly. of its serviced loans were in forbearance as of Dec. As of December 31, 1.3%

Yanling Mayer, Principal Economist at CoreLogic , recently revealed : “A distributional analysis of forborne loans’ payment status reveals that more than one third (39.1%) of all forborne loans are now 150+ days behind payment, while as many as 1-in-4 (25.5%) are 180+ days past due.”. Though 29.4%

P&I : Use a mortgage calculator to determine the monthly principal and interest on the loan. One-third of all sales were distressed properties (foreclosures or shortsales). Mortgage Rate : Look at the monthly 30-year fixed rate for June of that year as reported by Freddie Mac.

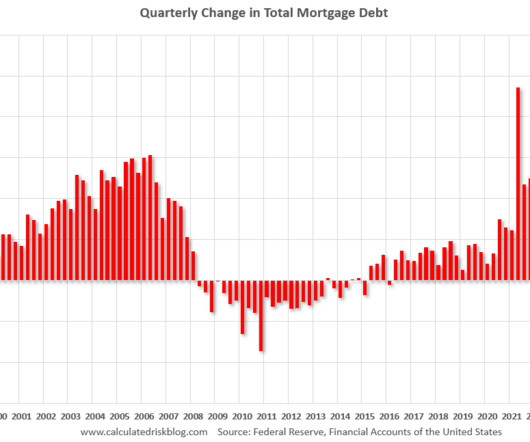

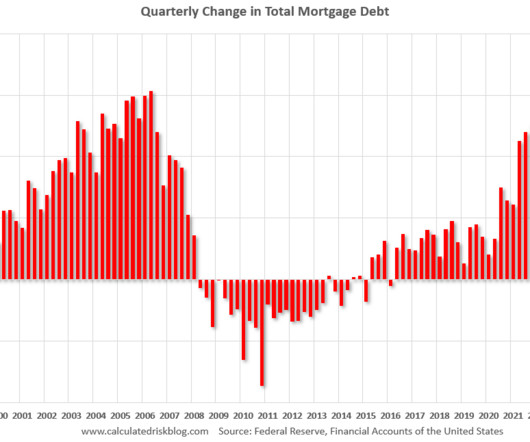

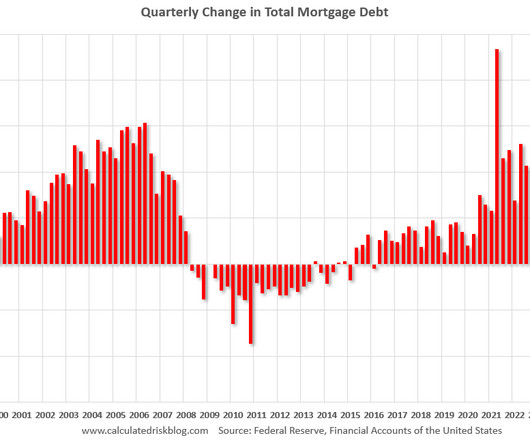

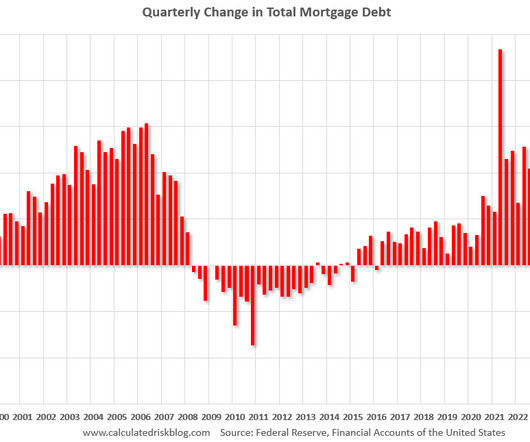

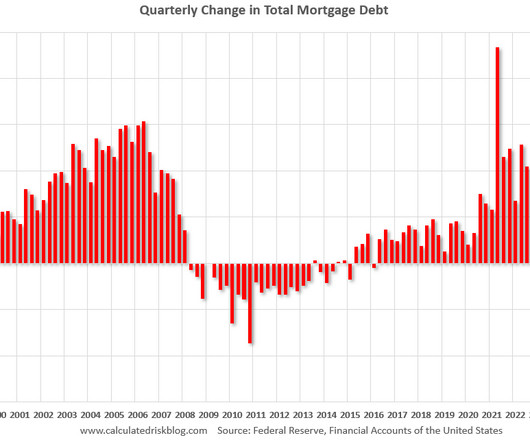

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. There are few debt cancellations now, so little MEW suggests that normal principal payments offset equity borrowing in Q2. 1 (sometimes called the Flow of Funds report) released today.

A defining term that emerged shortly after the collapse was the “shortsale”. In the years following, shortsales were the driving force behind a majority of all total real estate transactions. But what is the shortsale process and how does it work? . What is a ShortSale?

Experts who worked through The Great Recession of 2008 share how to handle tricky short-sale transactions. With its perfect storm of record-low property values and record-high unemployment, The Great Recession of 2008 triggered a rash of residential shortsales. Shortsales are not suited to all REALTORS ®.

But when it comes to one of the key aspects of buying that home — how to get a mortgage loan — you may draw a blank. We include advice from an agent who has worked with hundreds of new buyers, descriptions of different loans, and information about the many kinds of paperwork you’ll deal with. Source: (Matthew Henry / Burst).

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. There are few debt cancellations now, so negative MEW suggests that normal principal payments were greater than equity borrowing in Q1. 1 (sometimes called the Flow of Funds report) released today.

We talked to licensed real estate broker Christina Prostano , founder and principal agent of CP Global, who has been working the Manhattan and Brooklyn real estate markets in New York City since 2005. These are often called shortsales, and they’re just that - when a lender accepts a shortfall in the amount that is owed on the home.

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. There are few debt cancellations now, so little MEW suggests that normal principal payments offset equity borrowing in Q4. 1 (sometimes called the Flow of Funds report) released today.

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. There are few debt cancellations now, so little MEW suggests that normal principal payments offset equity borrowing in Q3. 1 (sometimes called the Flow of Funds report) released today.

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. Note the almost 7 years of declining mortgage debt as distressed sales (foreclosures and shortsales) wiped out a significant amount of debt.

However, in mid-2022, homeowners switched to using home equity loans (2nd loans) to extract equity from their homes. Note the almost 7 years of declining mortgage debt as distressed sales (foreclosures and shortsales) wiped out a significant amount of debt.

It happened faster than many predicted, with rates on 30-year fixed loans breaking through 5 percent in April to the highest level in more than a decade. As of July 11, 2022, interest rates jumped for all types of loans compared to a week ago. per month in principal and interest for every $100k you borrow. That’s an extra $7.56

We also connected with HomeLight Home Loans Mortgage Sales Leader Richie Helali, who offered an insider’s look at mortgage options that could help you hold on to your home — or let it go without falling into foreclosure. You’re maxed out on second loans and now you owe more than your home’s value. Negotiate a loan modification.

Even some homeowners of higher dollar homes have wound up in foreclosure: “I had one foreclosure where the house was worth over half a million, and it went into foreclosure over a loan of $10,000. If your sale proceeds won’t cut it, the next question is whether you could bring money to the table to cover those costs.

Here are a few of the details: Length of time: You must have used the home you are selling as your principal residence for at least two of the five years prior to the date of sale. It also does not have to be the two years immediately preceding the sale. of the loan amount. Expect them to run 1% to 1.5%

Like any investment, you don’t get profit if you hold it a short time.”. Here are some of the common concerns you may face: Cost of mortgage interest: At the beginning of your loan, a bigger percentage of your mortgage payment goes toward interest. of the loan amount. Expect them to run 1% to 1.5%

And by the time I moved back to LA, we were really in the throes of foreclosures and shortsales, so it was a different time completely. A 30-year fixed-rate loan, which is what a lot of buyers get, even though that doesn’t always make the most sense, but that feels safe for them. I started in D.C., So, you wait.

Make sure clients who see an acceleration clause in their mortgage contracts understand that this allows their lender to demand repayment of the loan in full if they default on the loan. 4 Loan Questions Worth Asking. Basically, amortization is the preset schedule of mortgage loan payments, including interest, over time.

We organize all of the trending information in your field so you don't have to. Join 144,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content