This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The combined cost of mortgages, taxes and insurance now takes up a larger share of household income than it has since the early 1980s, according to an affordability index from John Burns Research & Consulting. Department of Veterans Affairs (VA) loans, which made up 10%, according to purchase loan lock data from Optimal Blue.

These include insufficient credit or income, changes in credit scores and high debt-to-incomeratios. “A loan-to-value ratio that is too high, either because of a limited down payment or an appraisal of the home that resets the value used to calculate this ratio, can also be a factor,” she said.

housing market remains challenging for prospective buyers as concerns over mortgage rates , home prices and affordability persist in 2025. I believe the concerns for the market at this point are dramatically related to geographics. Jones, a Colorado-based LO for Lower -backed Universal Lending Home Loans.

Many who bought during the pandemic are now rethinking their decisions, citing changing lifestyles, financial miscalculations, and shifting market conditions, according to new data from Opendoor. Whatever that looks like, they’re kind of maxing out with the debt-to-incomeratio. They’re getting a loan.

In June, the bureau released two proposals regarding the QM Patch, which allows loans sold to Fannie Mae or Freddie Mac to exceed the 43% debt-to-incomeratio the Bureau had established in its Ability to Repay/Qualified Mortgage rule. Under § 1026.43(c)(2)(vii), Section 1026.43(c) ” (Bolding added by MBA.).

Nearly 1 in 5 millennials (19%) think their credit card debt will be a stumbling block when applying for a mortgage, while 1 in 7 (14%) think the same about their student loans. How student loans impact your ability to buy a home Adding a mortgage on top of monthly student loan payments can create a significant financial strain.

By making an offer of compensation, sellers communicate to buyers, as a marketing tactic, that their transaction costs may be reduced. They will continue to charge the highest price the market will bear, and leave buyers with an added up-front cost. High housing prices are caused by a housing shortage.

The San Francisco -based Unison calls its new offering the Equity Sharing Home Loan. The company explained that the product operates as a ”hybrid between debt and equity.” The product is a second mortgage with a below-market interest rate that allows a homeowner to tap into their equity without refinancing their existing mortgage.

A record 47% of government-sponsored enterprise (GSE) purchase loans in 2023 came from first-time homebuyers, a number that’s been trending gradually higher throughout the past decade. Looking back, last year’s market was dominated by purchase lending, with loans to buy homes making up 82% of a historically low number of originations.

He wants to know whether the potential borrower has acquired a buy now, pay later (BNPL) loan. And an underwriter told us that she was required by her lender to count the debts that were on the bank statement, including the BNPL loans.” Racamato promptly called some lenders he partnered with to ask how they deal with BNPL loans.

They’re centering on – there’s been a desire to move away from the so-called GSE Patch QM which is the Qualified Mortgage for loans that are held for sale to Fannie Mae and Freddie Mac that is scheduled for sunset on Jan. There are two proposals that came out in June. Q: What about the other proposals? But there would be other factors.

Over half of non-homeowning millennials (60%) say student loandebt is delaying them from purchasing a home, making them the population most affected by student debt , according to the National Association of Realtors’ 2021 impact of student loandebt report.

United Wholesale Mortgage (UWM), the nation’s largest wholesale lender, announced on Wednesday it will accept personal or business bank statements in self-employed borrowers’ loan applications. The product is available for loans up to $3 million and up to 90% loan to value. No mortgage insurance will be required.

Recent market trends — including an improvement in mortgage rates, housing affordability and potential refinance opportunities — suggest positive signs for the real estate market this year, according to February’s Mortgage Monitor report from Intercontinental Exchange (ICE). peak prior to the housing market downturn in 2006.

The Consumer Financial Protection Bureau is proposing a new category of qualified mortgages called Seasoned QM, which would require loans to meet certain performance requirements over a 36-month seasoning period. During the seasoning period, creditors would have to hold these loans on portfolio.

Although there is no doubt that business practice changes outlined in the National Association of Realtors’ (NAR) nationwide commission lawsuit settlement agreement are going to impact how real estate industry professionals operate, economists aren’t too sure they’ll have much bearing on the housing market. “I

The Consumer Federation of America (CFA) is calling for policy changes that would help alleviate the difficulties for homebuyers using Federal Housing Administration (FHA) loans when competing in tight markets. mortgage market in 2023, up from 14.3% of the U.S. in 2022, according to HUD.

HousingWire: How is today’s market shaping the need for a better customer experience particularly when it comes to closings? We’ve seen savings of up to 30% in difficult markets like Texas and Florida. In addition to finalizing a loan, there’s selecting movers, setting up utilities and more.

. “There’s been an explosion in high-DTI lending since I left FHFA,” he said, pointing to the fact that some Federal Housing Administration (FHA) borrowers have a 57% debt-to-incomeratio. DTIs on Fannie- and Freddie-backed loans have also risen, he said. “What we saw during COVID was the No.

And because their income didn’t keep up, lenders’ denials for a home loan jumped last year, according to a Consumer Financial Protection Bureau (CFPB) report released Wednesday. The CFPB report shows that the median total loan costs for home purchases was $5,952 in 2022, up 21.8% in 2022, up from 8.3%

The Federal Housing Finance Agency this week made a series of significant changes to loan level pricing adjustment (LLPA) fees charged by Fannie Mae and Freddie Mac on conventional/conforming mortgages. The changes include updates to pricing for second homes, high-balance loans and cash-out refinances that were first announced in 2022.

Tom Davis, chief sales officer, Deephaven Mortgage Today’s market means that more borrowers have higher debt-to-incomeratios, limited access to credit and are looking for alternative ways to get qualified for a mortgage. HousingWire: What factors are contributing to borrowers falling out of the Agency market?

A homebuyer’s guide to a competitive housing market. And unfortunately, prices are only going to continue to rise as the housing market remains strong. Your Income Is Stable. A stable income means you’re more likely to be approved for a loan , than someone with an unstable income. How are your finances?

Independent mortgage banks have been coping with a still-surging wave of loan-repurchase requests from Fannie Mae and Freddie Mac that represents yet another threat to lenders’ already stretched balance sheets. Those loans are going to be 20 points underwater, for the 3% to 3.5%

The repurchase-request volume, which includes both depository lenders and nonbanks, is being driven up this year by the huge volume of lower-rate loans made in 2020 and 2021 that Fannie and Freddie are continuing to vet for loan-sale representations and warranties violations. And it just might push some smaller lenders over the cliff.

So, start making money on every loan. Amid a challenging environment, Freedom has kept its cost structure low and has acquired loans to increase its servicing portfolio. According to Middleman, Freedom’s strategy allows the company to have a 30 basis-point cost to produce a loan. Guess what?

The decline was sharper for refinances when compared with purchase loans, according to the report. Most of the refinance originations left in the market were a small number of cash-out refinance loans. Despite rising rates that fueled this increase, debt-to-incomeratios did not see a significant change in the same period.

In this market where homes are selling like hot potatoes, it might seem like everyone can afford to buy a house, but that’s not true. And it doesn’t help that we’re living in a seller’s market where prices keep going up. A homebuyer’s guide to a competitive housing market. Step 2: Look At Different Loan Options.

Pontiac, Michigan-based United Wholesale Mortgage (UWM) capitalized on a booming private-label market in 2021 by sponsoring its inaugural securities transaction this past May, a prime jumbo deal involving 508 mortgages with an aggregate principal balance of $351.9 That’s a strong start for a new issuer. “A KBRA seems to think so as well.

million mortgage originations between 2012 and 2018 from Freddie Mac’ s Single-Family Loan-Level dataset, Haus found that the sweet spot for rates is typically in January, when mortgage originations also typically slump. An updated market outlook from Zillow expects seasonally adjusted home values to increase by 3.7% Analyzing over 8.5

Digital mortgage platform MAXEX , backed by investment from financial-services giant JPMorgan , sees a bright future in the ESG market. Originator interest in the Opportunity and Sustainable programs helped ESG loans make up 26% of loan volume traded through the exchange in November. “As Roelof Slump, managing director of U.S.

Following a chorus of complaints from the mortgage industry, the Federal Housing Finance Agency (FHFA) on Wednesday announced that it would delay the implementation of a new and controversial upfront fee on Fannie Mae and Freddie Mac borrowers with higher debt-to-incomeratios.

Kidwell said his company is looking for loan processors to identify fraud in non-QM loans, in addition to loan officers. The hiring trend at non-QM lenders stands in sharp contrast to recent layoffs at some consumer-direct lenders, which specialize in conventional refinance loans. trillion in 2022.

This implies easing inflation next year, and mortgage rates near 6% would help affordability issues caused by two things: The inflation fight has fueled the mortgage rate spike Low inventory and a steady job market have put a floor on home prices The good news is that GSEs remain committed to loan approval guidelines that help in these tough cycles.

The Urban Institute regularly cites statistics showing IMBs do a better job than banks of serving underserved borrowers, as measured by metrics such as FICO scores and debt to incomeratios. Unlike banks, IMBs don’t have access to Federal Home Loan Bank advances that help banks fund mortgage loans.

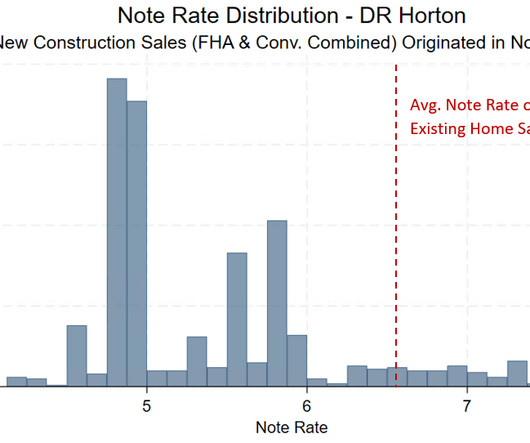

While sellers of existing homes have struggled with rising rates and softening demand, homebuilders have not only survived, but thrived in this market thanks to the use of mortgage rate buydowns , a tool more widely used by builders since their business is selling homes and clearing inventory. Source: AEI Housing Center, www.AEI.org/housing.

The move is part of a legal battle that started in September 2021 when Richards filed a lawsuit alleging the lender closed thousands of loans without proper documentation to boost its performance ahead of its initial public offering (IPO) on the New York Stock Exchange. But “instead, Richards crumbled.”

The recent offering , CAS Series 2022-R02, involves transferring loan-portfolio risk to private investors via a $1.2 billion note offering backed by a reference pool of 149,393 residential mortgage loans valued at $44.3 trillion in single-family mortgage loans, measured at the time of the transaction. billion.

As market volume dips and pent-up demand builds, 61% of millennials and Gen Zs who intend to buy a home plan to apply for a mortgage this year. For years, the dominant market narrative defining these generations has been digital-first experiences and poor financial habits. Creative paths to homeownership in a challenging market.

The Mortgage Bankers Association sent a letter on Monday to the Consumer Financial Protection Bureau asking for a six-month extension to the so-called “GSE patch” that allows Fannie Mae and Freddie Mac home loans to borrowers with high debt levels to be considered Qualified Mortgages.

HousingWire recently spoke with Matic CEO and co-founder Ben Madick about the changing home insurance market, how it impacts mortgage lenders and homeowners, and why lenders should pay attention. HousingWire: What is the current home insurance market like? In 2022, property and casualty insurers recorded a combined ratio of 102.4%

One key issue is the PSPA amendment that limits Fannie Mae and Freddie Mac from buying single-family loans secured by investment properties or second homes. The MBA notes that the PSPA’s lack of clarity may have already generated negative market impacts, outlining four specific areas of concern: 1.

LendingLife is a daily digest of the most important news and commentary edited and curated exclusively for mortgage loan originators. Asked pointedly about whether he supported the rule, Chopra answered “I don’t know,” and changed the subject to how the CFPB could spur refinances in the market. Join the community ! Hello, LOs!

The final rule established a pricing threshold that effectively replaced the debt-to-income limit of 43% with a price-based approach that gives lenders relief for loans capped at 150 basis points above the prime rate. Presented by: Proctor Loan Protector. “As

We organize all of the trending information in your field so you don't have to. Join 144,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content